[Natural Rubber]: Rubber Daily Journal (August 5)

Analysis of natural rubber market price on August 5

index

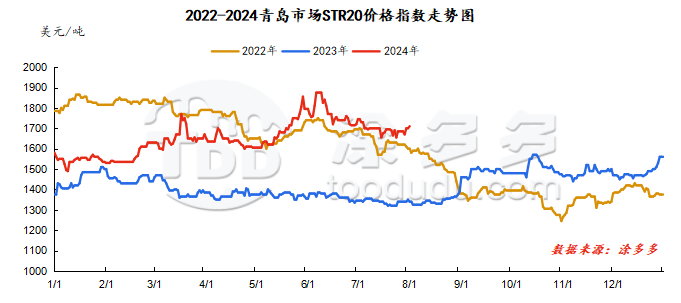

August 5June, Natural Rubber Qingdao Market STR20 Price Index1740 USYuan/ton, compared withThe previous trading day rose by US$30/ton.

market analysis

market analysis

futures market

spot market

Supply:

Foreign countries: There is more rainfall in northeastern Thailand than in the south, and there is still more rainfall overall, which affects the pace of new rubber release. Restocking by secondary suppliers is not smooth, and there is not much room for downside in raw material purchase prices.

Domestic: Currently, Yunnan production has been fully cut, and glue has entered the stage of comprehensive supply. Recently, there has been frequent rainfall in the production area, less glue has been collected, and raw material prices have stabilized.

Typhoon weather in Hainan's production areas has eased, raw materials are expected to be stored, and the actual purchase price of raw materials has dropped within a narrow range.

Demand side:At present, the start-up of all steel tire sample companies is differentiated, and the start-up performance of front-line brands is stable. Most enterprises in Shandong flexibly control production based on their own shipments and inventory conditions. At present, some pre-maintenance companies have started to return to normal, and some companies are still in the maintenance stage. At the beginning of the month, the overall shipment performance was average. In terms of the market, market demand is flat and trading is average. I heard that the price policies of some brands have been lowered, and some support has been given to some specifications. Overall, there are no obvious companies in the market demand, and purchases through channels are cautious, and a wait-and-see situation is temporarily maintained.

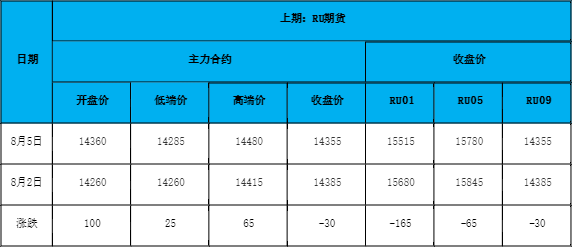

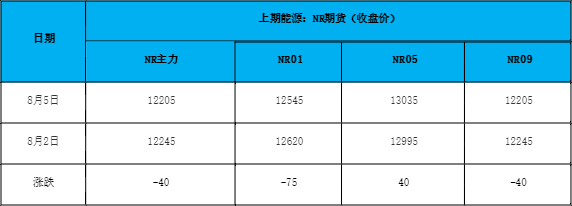

Futures spot price list

market outlook

Recently, the positive driving force of the main rubber contract is not obvious for the time being. From the perspective of supply, expectations for the increase in raw materials have begun to strengthen. After entering August, supply pressure in the production areas will continue to increase, and expectations for a decline in cost-side support will strengthen. The off-season for downstream demand is approaching, and the overall start-up of enterprises remains weak. The overall data is still in a dismal state. The willingness to purchase raw materials has cooled down. The social inventory of natural rubber may continue to accumulate. It is difficult for both supply and demand to provide significant support for rubber prices. It is expected that short-term natural rubber is basically in a state of slow change, with more narrow fluctuations.